In 2026, the global FinTech market is expected to reach about $460 billion, with steady double-digit growth projected for the next decade. Financial services are no longer tied to banks – they are built into apps people use every day. The shift is already measurable.

This creates real pressure for businesses. Users expect instant payments, simple onboarding, and full control within the app. Products that fail to deliver this are replaced fast.

FinTech app development is how companies respond. It enables businesses to build a fintech app that processes payments, manages lending, and handles financial data in real time. In a market where users expect everything within the app, speed and trust become the only real advantages.

What is a FinTech App and Why Build One?

Not long ago, managing money meant queues, paperwork, and slow approvals. Opening an account could take days. Sending money abroad – even longer. Today, one app replaces all of that.

A FinTech app is a digital product that lets users manage money, make transactions, or access financial services directly from a phone. It can be a banking app, a payment tool, or a platform for investments or lending applications. Everything happens within the app – fast and without friction.

For businesses, the reason to build a fintech app goes beyond convenience. It reduces operational costs, automates complex financial processes, and opens access to new markets. A well-designed fintech product improves user experience and builds trust, which directly impacts retention and revenue. In a market where speed wins, a strong app often becomes the entire business.

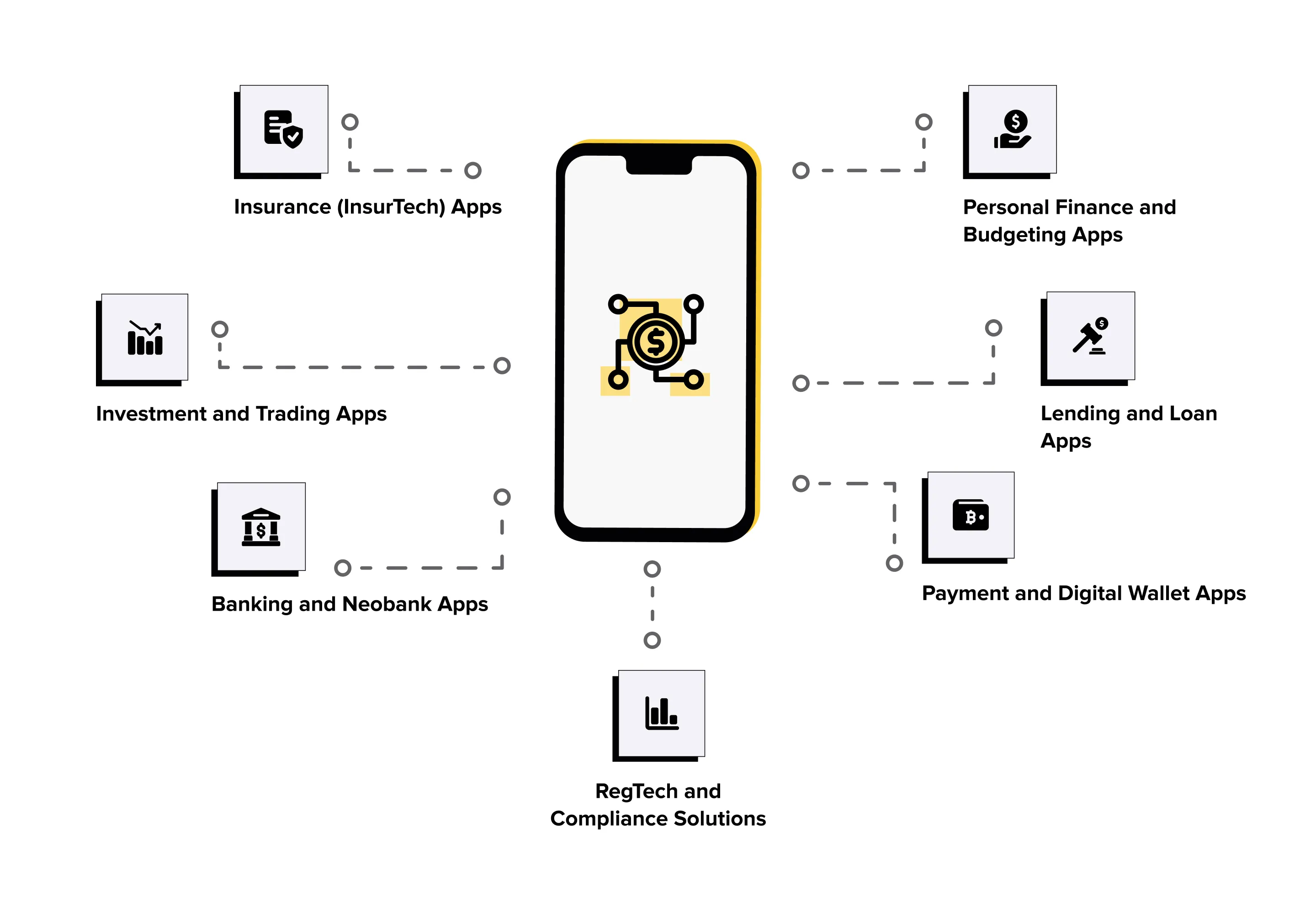

Types of fintech apps

FinTech is not a single product – it’s a set of solutions built around different business goals and user needs. Some apps focus on payments; others on lending, investing, or compliance; and many combine several services into a single fintech product. The right format depends on what problem you solve and how users interact with money within the app, which is why understanding these categories helps define your product strategy early.

Banking and Neobank Apps

Banking apps and neobanks replace traditional branches with a fully digital experience, allowing users to open accounts, manage cards, and conduct transactions without visiting a bank branch. A modern banking app provides instant access to balances, transfers, and financial services 24/7, while neobanks operate without physical offices and focus on speed, lower fees, and simple onboarding. This model helps fintech companies reduce costs and improve user experience, which is why many users switch from traditional banking to mobile-first solutions.

Payment and Digital Wallet Apps

Payment and digital wallet apps simplify the way users send, receive, and store money, replacing cash and cards with mobile payments. They support peer-to-peer transfers, contactless payments, and online purchases, making transactions faster and more convenient. Security is built into the process through encryption and tokenization, which protects sensitive data during payment processing. These apps are widely used for everyday payments, from shopping to splitting bills.

Lending and Loan Apps

Lending applications give users quick access to credit without the delays of traditional banks, using automation and alternative scoring instead of manual checks. These lending apps process requests faster, often within minutes, and offer flexible options like short-term loans or BNPL services. For users, this means easier access to funds, while for businesses it creates new revenue streams, though risk management and fraud detection remain critical.

Investment and Trading Apps

Investment apps allow users to manage assets like stocks, crypto, or funds directly from their smartphones, making investing more accessible to a wider audience. These platforms offer portfolio tracking, real-time trading, and sometimes robo-advisory features that automate decisions based on data. While they simplify entry into financial markets, users still need to understand risks, as market volatility directly affects returns.

Personal Finance and Budgeting Apps

Personal finance apps help users track income, expenses, and financial habits, providing a clear view of where money goes and how to manage it more effectively. These tools connect bank accounts, analyze spending, and provide insights that support smarter decisions. Many apps also automate budgeting and offer personalized recommendations, which improve financial awareness and help users plan long-term goals.

Insurance (InsurTech) Apps

InsurTech apps simplify the way users buy and manage insurance by digitizing policies and claims. They allow users to compare offers, purchase coverage, and submit claims faster, while automation reduces processing time and personalizes services based on user data.

RegTech and Compliance Solutions

RegTech solutions focus on helping businesses meet regulatory requirements by automating processes like KYC, AML, and fraud detection. These tools are primarily used by financial institutions and fintech companies to reduce manual effort, improve accuracy, and mitigate compliance risks. By centralizing reporting and monitoring, they help organizations stay aligned with regulations while lowering operational costs.

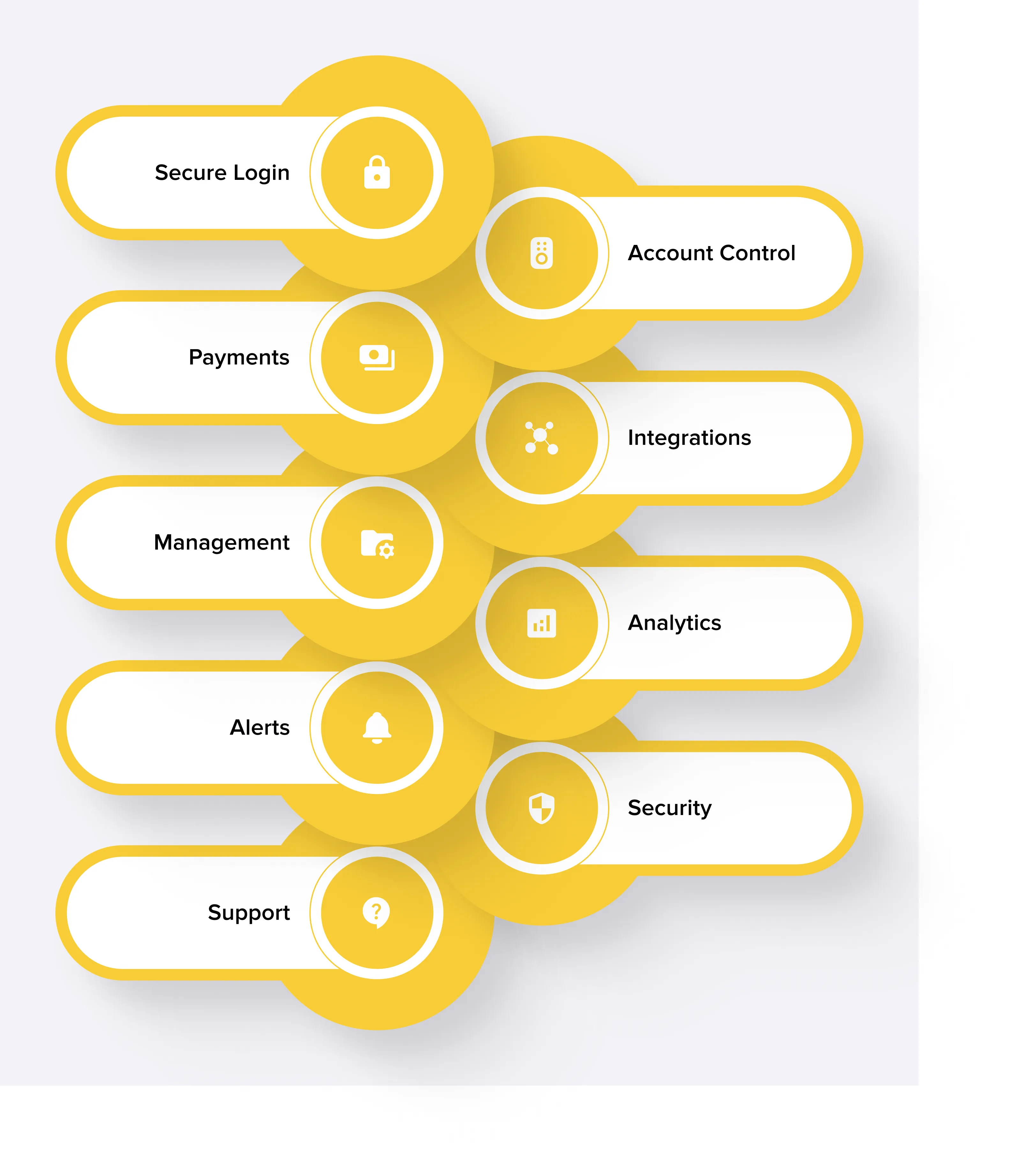

Must-Have Features of a FinTech App

When you build a fintech app, features are not just about functionality – they define trust. In most apps, a missing feature affects user experience, but in FinTech, it affects whether users stay at all. If something feels unclear, slow, or unsafe, people leave immediately. That’s why every successful fintech app combines strong security, clear UX design, and reliable financial functionality to create a product users can trust from the first interaction.

Secure Authentication and User Authorization

Secure access is the first layer of trust in any fintech app, which is why authentication typically combines login credentials with biometric and two-factor verification. This approach protects accounts from unauthorized access and reduces fraud risk, especially during sensitive operations such as transactions. Strong authentication not only keeps user data safe but also helps businesses meet compliance requirements and build user trust from the very first login.

Account and Card Management

Users expect full control over their finances within the app, including real-time balance tracking, card management, and transaction history. A well-designed banking app allows users to block cards, set limits, or manage multiple accounts with a few taps, improving transparency and reducing friction. This level of control helps users feel confident about their finances and makes the app a central tool for everyday financial activity.

Payments and Money Transfers

Payments are the core of most fintech products, allowing users to send money, pay bills, and complete international transfers with minimal friction. A reliable fintech app ensures fast transaction processing, clear status updates, and stable performance, as even small delays can erode user trust. Many businesses partner with a fintech development company to build secure payment flows and support flexible payment options, which often become a key reason why users choose one app over another.

Integration with Payment Gateways and APIs

To build a fintech application that works under real-world conditions, integration with payment gateways and APIs is essential, as it connects the app to banks and external services. These integrations support payment processing, account verification, and data exchange, while also making it easier to scale and expand into new markets. Teams with experience in banking software development usually handle these integrations more efficiently, reducing risks and ensuring the app meets both technical and compliance requirements.

Personal Finance Management and Analytics

A fintech app provides more value when it helps users understand their financial behavior, not just track it, which is why personal finance tools analyze spending, categorize transaction data, and offer insights based on real usage. This improves decision-making and helps users plan budgets more effectively, while personalization enhances the overall user experience and builds long-term engagement.

Custom Notifications and Alerts

Real-time notifications keep users aware of every transaction, spending update, or security event, helping them react quickly if something looks unusual. At the same time, personalized alerts improve relevance and reduce noise, ensuring users receive only meaningful updates. In products like cashback app development, notifications also play a key role in engagement by informing users about rewards, offers, and activity within the app.

Security and Data Protection

Security and compliance are critical in any fintech app, as users trust the platform with sensitive data. To protect it, developers use encryption, secure infrastructure, and fraud detection systems that monitor activity in real time. Meeting security and regulatory compliance standards is essential for building a reliable fintech solution and maintaining user trust.

Customer Support and Assistance

Even a well-built fintech app needs accessible support, since financial issues require fast responses and clear guidance. Most apps combine live chat, FAQs, and AI tools to resolve problems quickly and improve the overall user experience, while also helping your business build trust and retain users over time.

Steps to create a fintech application

Many teams try to build a fintech app fast and jump straight into development. This is where most projects fail. In fintech, delays rarely occur due to coding. They happen because key steps were skipped – compliance was not planned, integrations were not ready, or the product had no clear direction.

To develop a fintech app that actually launches, every stage must connect to the next. A structured process helps avoid rework, reduce costs, and ensure the app meets security and regulatory compliance requirements from the start. This is the difference between an idea that stalls and a successful fintech app that scales.

Step 1: Define Your FinTech Niche and Business Goals

To build a fintech application, start with a clear niche. The fintech industry is competitive, and broad ideas rarely work. Banking app products, lending apps, and payment platforms already dominate the market.

Focus on a specific problem. It can be faster payment processing, better fraud detection, or easier access to financial tools. A strong fintech product solves one problem well instead of many problems poorly.

Then define your business goals. Decide how your app provides value and generates revenue. Without a clear model, building a fintech app becomes unpredictable and difficult to scale.

Step 2: Research Regulations and Ensure Compliance

Before you create a fintech, understand all compliance requirements. This includes KYC, AML, GDPR, and PCI DSS standards.

These rules define how your app handles authentication, user data, and transactions. Ignoring them leads to legal risks, blocked operations, and loss of user trust. A reliable fintech product always starts with strong security and regulatory compliance.

Step 3: Plan Features and Create a Product Strategy

When teams build fintech app solutions, they often try to launch a full-featured product too early. This increases cost and slows down development. Start with an MVP and focus on must-have features such as authentication, account access, payment gateways, and the core transaction flow. A clear roadmap helps prioritize updates.

Step 4: Design UI/UX for Trust and Simplicity

When you make the app, user experience defines success. Financial apps must be clear and predictable. Users need to understand balances, transactions, and actions without confusion. Strong UX design simplifies flows, improves onboarding, and builds user trust. If the interface feels complex, users leave – even if the functionality is strong.

Step 5: Choose the Right Tech Stack and Architecture

To build a fintech app that scales, you need technology that supports growth and stability. Backend systems must handle large volumes of transactions without delays. APIs allow smooth integration with banks, payment gateways, and external services.

Cloud infrastructure adds flexibility, while tools like React Native help support iOS and Android faster. Still, performance and security should always come first. Poor architecture leads to system failures, slow performance, and high long-term costs.

Step 6: Develop the App and Integrate Payment Systems

At this stage, you build a fintech app in practice by combining all features into a working system. Development focuses on stability and accuracy.

Payment processing becomes the core functionality. Integration with payment gateways and banking APIs must be seamless. Users expect fast and reliable transactions within the app. Security measures like authentication, encryption, and two-factor authentication protect every interaction.

Step 7: Test for Security, Performance, and Compliance

Testing is a critical part. You need to check performance under load, validate compliance with requirements, and test systems such as fraud detection. Even small issues can lead to failed transactions or security risks, so regular audits and testing ensure the app delivers stable, secure performance.

Step 8: Launch, Monitor, and Improve

When you create a fintech app, launch is only the starting point. Publishing the product does not guarantee success.

After release, monitor how users interact within the app. Track transactions, detect errors, and analyze behavior. This data helps identify weak points and improve user experience.

A fintech app that scales evolves constantly. Updates, new features, and performance improvements help your product stay competitive and expand into new markets.

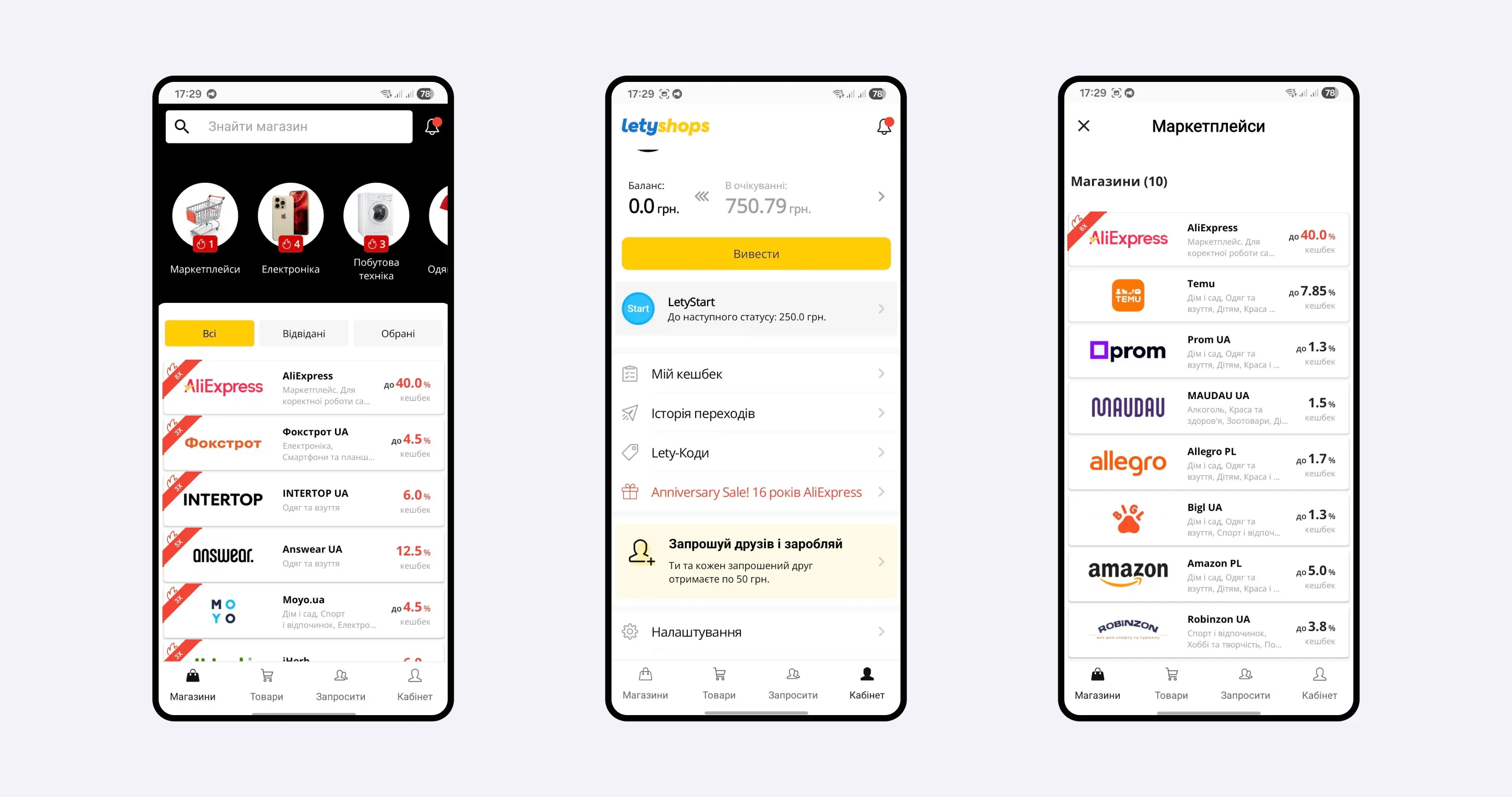

Real-World Example of FinTech App Development

One case shows how building a fintech app works beyond theory. LetyShops, a cashback platform, needed to scale fast as user traffic grew across multiple markets. The product handled thousands of daily transactions, but performance drops and slow updates started to affect user experience.

The main challenge was clear: keep the app stable while expanding features and integrations. The Lampa team focused on backend optimization and improved the way transaction data was processed. We also rebuilt parts of the system to improve scalability and enable smoother integration with partner stores.

On the front end, UX design changes made navigation simpler and reduced friction in the cashback flow. Users could track rewards and transactions within the app with fewer steps.

As a result, the platform handled higher loads without delays, and user engagement improved. This is what a scalable fintech product looks like in practice – steady performance, clear UX, and the ability to grow without breaking.

Challenges of FinTech App Development

Most teams underestimate where things actually break. It’s rarely the idea – it’s everything around it. Regulatory requirements like KYC, AML, and PCI DSS often become hidden blockers. When compliance is treated as a late step, projects stall before launch or require costly rework. Security adds more pressure. A fintech app that feels unsafe loses users quickly, and weak authentication or poor fraud detection usually only becomes apparent under real load.

Integrations create another layer of risk. Payment gateways, banking APIs, and external services don’t always work as expected, and each connection can delay release or affect stability. Then comes user trust. Even small UX issues – unclear transactions, missing details, or late notifications – raise doubts. In FinTech, doubt spreads quickly, and once trust is lost, users rarely return.

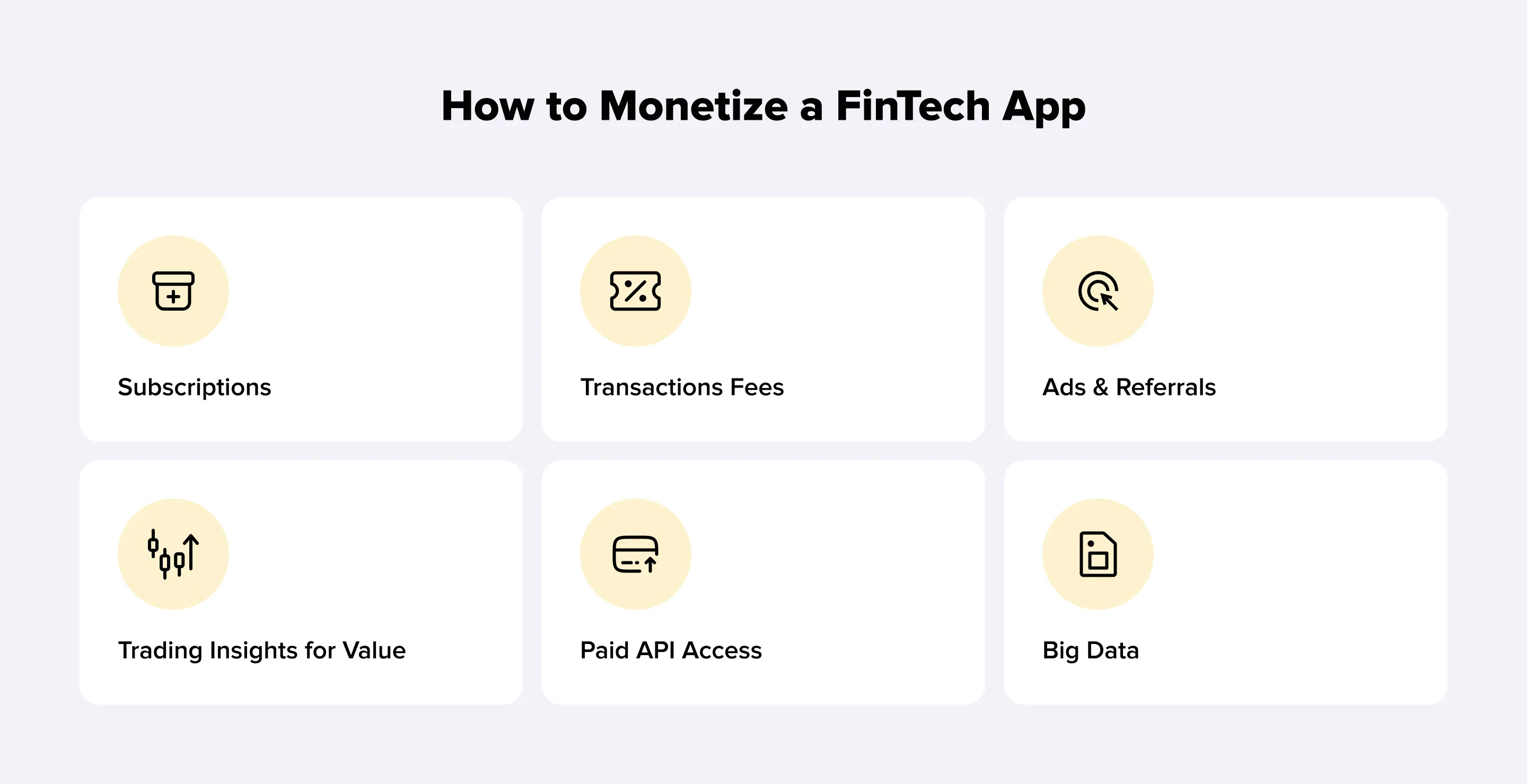

How to Monetize Your FinTech App?

Monetization in FinTech is usually tied to how money moves inside the product. Payment apps often take a small fee per transaction – the same model used by companies like Stripe. Neobanks follow a different path. Products like Revolut offer free plans but charge for premium tiers with extra features.

Investment apps use commissions or margin trading. Robinhood, for example, earns from premium services and trading mechanics rather than simple usage. Lending apps make money through interest or service fees.

The key is simple: the model should match how users interact with your product. If the app provides frequent transactions, the fees work. If it offers value over time, subscriptions make more sense.

How Much Does It Cost to Build a FinTech App?

The cost of fintech app development depends on the product's complexity. A simple MVP with basic features costs much less than a full-fledged fintech platform with integrations, security layers, and compliance requirements. Features, payment gateways, and the location of the development team all affect the final price.

Here’s a rough breakdown:

Product Type | Product Type |

MVP | $40,000 – $80,000 |

Mid-level product | $80,000 – $150,000 |

Complex platform | $150,000 – $300,000+ |

These numbers reflect typical financial software development projects with standard functionality. If you plan to build a fintech app that scales, costs grow with integrations, security, and performance requirements.

Every product is different. The fastest way to get a clear estimate is to define your launch idea and request a tailored calculation from Lampa. Get in touch with our team.

Conclusion

Strong FinTech products don’t appear by chance. They are built step by step – with a clear idea, a real market need, and careful decisions at every stage. Teams that succeed treat development as more than coding. They think about compliance early, design for trust, and plan how the product will scale from the start.

To build a fintech app that works, you need to balance speed with stability. Launch fast, but don’t skip the parts that protect users and the business. The difference between a product that grows and one that stalls is rarely the idea – it’s how well each decision supports long-term value.

FinTech is still expanding. The opportunity is there, but only for products that solve real problems and earn user trust from day one.